Before we continue, we are talking about a "term" insurance:

Term is a type of life insurance that provides a potential death benefit for a fixed period or "term." This is commonly a flat premium for say, 5, 10, 15, 20, or 30 years. After the end of the term the policy no longer provides a death benefit

Source: https://www.investopedia.com/ask/answers/08/term-life-insurance.asp

To add, it has no cash values at the end of the term. It's just like your car or mortgage insurance or even your electronic good insurance (fridge, washing machine, etc.).

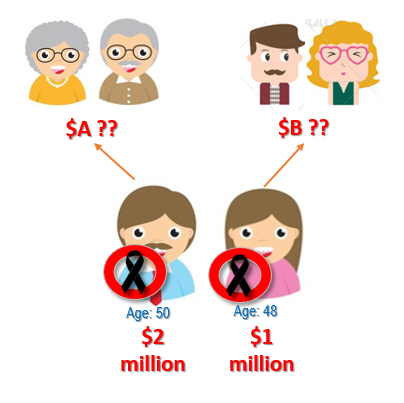

Do I need a million dollar coverage? Well it depends.

Below are 3 commonly consideration you might want to take note:

A) Current Debts (house, car, etc.)

Do you know that you can use Term insurance to replace your HDB's Home Protection Scheme (HPS)? With this Term plan also, you do need to get a new HPS when you get a new house, which is usually more expensive because the HPS is based on your current age and not the younger you whom 10 or 20 years ago took up HPS when you got your first house.

B) Family regular living expenses

You can just use your monthly expenses and multiply by the number of years you need to support your family.

E.g. A new born just join the family and assuming your monthly expenses is $2,000. So for the new born to be independent, we assume he/she will take about 25years. So we just multiply accordingly: $2,000 x 25y x 12m = $600,000.

C) Children Education

For a 3 years course in a local universities (NUS/NTU), based on inflation rate of 5%, in 20 years time, the course fee will come to about $71,000. If we add in the living expenses with an inflation of 1.6%, the grand total comes to $142k.

And if we are talking about overseas education, like Australia, the total cost will come to $440k

Still unsure if you really need the $1mil coverage? Talk with your financial advisor and they are the best person to advise you.