If you don't have Eldershield nor coverage for Acitivites Daily Living, you can still be covered under Aviva which has a Guaranteed Issuance Offer (GIO) plan.

If you already have coverage for ADL, then how about simplified coverage for loss of use of one limb OR loss of sight of one eye OR loss of speech OR loss of hearing from NTUC Income which is also a GIO plan?

Showing posts with label 05 Wealth Distribution. Show all posts

Showing posts with label 05 Wealth Distribution. Show all posts

23 November 2017

15 November 2017

Advance Medical Directive (AMD)

An Advance Medical Directive (AMD) is a legal document that you sign in advance to inform the doctor treating you (in the event you become terminally ill and unconscious) that you do not want any extraordinary life-sustaining treatment to be used to prolong your life.

Making an AMD is a voluntary decision. It is entirely up to you whether you wish to make one. In fact, it is a criminal offence for any person to force you to make one against your will.

Source: MOH

The AMD must be made through a doctor (you do not need either a lawyer or legal advice to make an AMD). The doctor has the responsibility to ensure that:

1. You are not being forced into making the AMD.

2. You are not mentally disordered.

3. You understand the nature and implications of making an AMD.

You need to have two people witness you sign the AMD and they must sign the form as witnesses in your presence. One witness must be the doctor. The second witness must be 21 years or above and can be the doctor’s nurse, or any other suitable person.

If the witnesses are relatives, so long as they have no vested interests in your demise, they would be allowed to act as witness.

Since it's a requirement to get doctor to certify, it's best to do it during LPA application.

Making an AMD is a voluntary decision. It is entirely up to you whether you wish to make one. In fact, it is a criminal offence for any person to force you to make one against your will.

Source: MOH

The AMD must be made through a doctor (you do not need either a lawyer or legal advice to make an AMD). The doctor has the responsibility to ensure that:

1. You are not being forced into making the AMD.

2. You are not mentally disordered.

3. You understand the nature and implications of making an AMD.

You need to have two people witness you sign the AMD and they must sign the form as witnesses in your presence. One witness must be the doctor. The second witness must be 21 years or above and can be the doctor’s nurse, or any other suitable person.

If the witnesses are relatives, so long as they have no vested interests in your demise, they would be allowed to act as witness.

Since it's a requirement to get doctor to certify, it's best to do it during LPA application.

13 November 2017

FAQ on LPA

What is the difference between a Will and a LPA (Lasting Power of Attorney)?

A Will is effective only after death. A LPA is effective when you loose mental capacity e.g. when one is in coma or dementia.

What happens if I do not have a LPA?

Your family members will have to apply to Court under the Mental Capacity Act, to apply for someone to take charge of your personal welfare and property & affairs matters. Somewhat similar to someone without a Will, it's costly and time-consuming and you do not get to choose who's best to take care for you.

Can I assign my spouse to take care of my healthcare whereas my son to take care of my financial matters?

Yes. Basically LPA allows you to assign the following decision making:

1) personal welfare (which may include health care) and/or

2) property and affairs (including financial matters).

3) both personal welfare and property and affairs

So it's best to decide who's best to manage your healthcare and financial matter.

What happen if the assigned is not taking care of my affairs irresponsibly?

The Office of Public Guardian has the power to oversees the assigned do their job responsibly. If they don't they are held responsible and in worst case be fine and imprisoned.

What happens if I recover my mental capacity?

The LPA will not be effective. It's only effective when you are certified to be incapable of managing your own affairs.

Will my LPA be revoked or cancelled in any condition?

Yes, if the person you assigned decline to take the job, passes away, bankrupt or he himself lost mental capacity.

If the assigned is your spouse and there is a divorce.

Other than LPA, anything else I need to consider?

LPA is effective only when you lost your mental capacity. Upon death, LPA is of no use. Will is the only effective tool to help you.

9 November 2017

What is Lasting Power of Attorney (LPA)

The LPA is a legal document which allows a person who is at least 21 years of age ('donor'), to voluntarily appoint one or more persons ('donee(s)') to make decisions and act on his behalf should he lose mental capacity one day. A donee can be appointed to act in the two broad areas of personal welfare and property & affairs matters.

Benefits of an LPA

Source: Office of the Public Guardian

Do you know that the application is free at this moment:

However applicants are required to pay a fee to engage an LPA Certificate Issuer to witness and certify their application. We last checked it was only $60 from a a medical practitioner accredited by the Public Guardian.

Please note that LPA application must be within 6 months from the date the certificate issuer signs on the LPA.

Click here to find out more who can certify your LPA.

Benefits of an LPA

- Early preparations to protect your interests should one become vulnerable one day.

- Enables you to make a personal, considered choice of a trusted proxy decision maker, who is reliable and competent to act in his or her best interests.

- Alleviates the stress and difficulties faced by loved ones who need to apply for a Deputyship order, if you lose mental capacity without an LPA in place.

Source: Office of the Public Guardian

Do you know that the application is free at this moment:

(fee of $75 waived for another 2 years until 31 August 2020)

However applicants are required to pay a fee to engage an LPA Certificate Issuer to witness and certify their application. We last checked it was only $60 from a a medical practitioner accredited by the Public Guardian.

Please note that LPA application must be within 6 months from the date the certificate issuer signs on the LPA.

Click here to find out more who can certify your LPA.

1 November 2017

What can I use SRS for? Not just leave it in the bank until I retire?

Now that I have save $1,756 on my tax for YA2018 with SRS (Supplementary Retirement Scheme), next year I got additional money to spend/ save/ invest. (Click here for the previous article on Tax Savings details).

Then how about the $15,300 I left it in the SRS account?

Well, with SRS you can do alot of things as it's as good as cash (in terms of investment wise).

1) Option 1

Well I have already saved & earned 11.5% with the tax savings, I'll just let it grow 0.5% yearly until I retire.

1) Option 1

Well I have already saved & earned 11.5% with the tax savings, I'll just let it grow 0.5% yearly until I retire.

=> Leave it in the bank and don't need to do anything.

Then how about the $15,300 I left it in the SRS account?

Well, with SRS you can do alot of things as it's as good as cash (in terms of investment wise).

=> Leave it in the bank and don't need to do anything.

2) Option 2

I am a long term investor (or speculator, I wonder?) and would like to try my hands on current market high as there's still 30% of chances going up.

=> Link your SRS with your Stocks account, and you can start speculating.. I mean investing.

3) Option 3

I am a bit risk averse but I believe in stocks as it has always been and historically shown to beat the inflation. But which stocks to buy?

=> Invest in equities or balanced funds instead. E.g. of balanced fund "First State Bridge"

4) Option 4

I don't trust stocks and shares. I only believe in Corporate Bonds issued by reputable companies and Statutory Bonds issued by Singapore government. But I don't have $250,000 to buy them.

=> Invest in money market or bond funds instead. E.g. "United SGD Fund CL A ACC SGD"

Getting confused and not sure which option to choose? Perhaps it is good to know your own-self first before making any decision that you might regret. Check out this month article too on "Understand Yourself before making that Investment Decision"

5) Option 5

What? Still got Option 5?? I start seeing seeing stars already. I just want a stable retirement and it's best if I can use my SRS to pay myself when I'm retired or no longer working. Got such thing?

=> Fortunately yes! There are insurers who allows you to use your SRS to pay for their retirement plans. In fact nowadays almost all retail life insurers have at least 1 retirement plan in the market.

Check out below the available plans that you can use your SRS:

6) Option **

Now I really see stars and totally lost. I think I will go for Option 1, easiest. Let it grow for 20years from $30k to $33k and earn $3,000, guaranteed. Not bad as I don't even need to lift my fingers.

=> How about earning a guaranteed $7,200 and another ~$16,000 for your play cheque? In addition, you have extra protection for death & terminal illness for the "just in case". But this you need to lift your finger and just give us a call and we will advise you based on your risk appetite. Oh.. not only lifting of fingers but need to use your mouth to talk a bit also ya :)

25 October 2017

TST: Wealth Management: Views on Financial Planning and Money Management

Below is the screen capture from the Sunday Times earlier this week:

You can notice that for Retirement Planning, more than 70% wants their retirement fund to be enough to maintain current lifestyle and their family is well protected and provided for when they retire.

And the Top 4 topics where investors need more information is:

1) Writing a Will

2) Lasting Power of Attorney (LPA)

3) Estate Planning

4) Succession Planning

For Writing a Will with 78% requiring more information, we have ample information about it in this blog, check this out especially:

1) Does everybody have a Will?

2) FAQ on Will

3) CheatSheet : Estate Distribution

As for the LPA, we will be sharing what is LPA and the FAQs about LPA next month.

If you need any clarification, feel free to contact us.

You can notice that for Retirement Planning, more than 70% wants their retirement fund to be enough to maintain current lifestyle and their family is well protected and provided for when they retire.

And the Top 4 topics where investors need more information is:

1) Writing a Will

2) Lasting Power of Attorney (LPA)

3) Estate Planning

4) Succession Planning

For Writing a Will with 78% requiring more information, we have ample information about it in this blog, check this out especially:

1) Does everybody have a Will?

2) FAQ on Will

3) CheatSheet : Estate Distribution

As for the LPA, we will be sharing what is LPA and the FAQs about LPA next month.

If you need any clarification, feel free to contact us.

23 October 2017

FAQ on Will

Below are some of the FAQs that we received from our friends and clients. If you have any queries, please feel free to let us know or just drop us a comment below.

Can I make my own will?

Yes, you can. But it's not recommend. It's best left to the professional.

E.g. if you owned a Lexus and would like to pass it to your son when you passes on. In your Will, you indicated "to give Lexus car to my son". If you have changed your car to BMW, upon your demise, your executor will need to sell your BMW and purchase a Lexus for your son.

Being smart alec, you rephrase it to "to give a car to my son". But then if you have sold your car and/or bought a yacht, then the executor will need to find monies or sell your yacht to buy a car for your son.

What can I put into the Will?

Basically you can put all your estate in your Will except those governed by the law. Refer to the Cheat Sheet here for quick reference on what can and cannot be distributed by law.

How about estate that is overseas?

Estate is divided into 2 types: Movable and Immovable Estate.

For movable estate such as overseas bank accounts, investment, etc. it can be distributed via your Will locally here.

For immovable estate such as overseas properties, land title, etc. it's best to do up a will at the respective country. Immovable estate are usually governed by the respective country's laws.

Is it possible that my Will be revoked?

Yes, when you marry or re-marry unless it's mentioned in the Will.

How about if I'm divorced?

No, divorce does not revoke your Will. So do update your Will promptly after change in marital status.

To add-on, without a Will, even after you file for divorce, the Intestate Succession Act (where you spouse is entitled to HALF of ALL your properties) continues to apply until the date of Final Judgment.

And your spouse also have the FIRST RIGHT to apply for the letter of the administration from the court to deal with all your estate!

Is the Will best kept in a safe place e.g. Bank Safe?

Yes, it should be kept in a safe place but it's a no no to keep in the Bank Safe. Because no one other than yourself has the access to the Bank Safe. However you can consider keeping it in a "fire proof" safe deposit box at home.

Since the Executor needs it to carry out your Will, it would make sense that the Will should be made known where it is especially for the Executor and/or Beneficiaries. If not, you can consider registering your Will location at the "Will Registry" maintained by the Public Trustee of Singapore.

If the Will cannot be found, then the estate will be distributed based on the The Intestate Succession Act.

Other than Will, anything else I need to consider?

Will is effective only upon death. If one is diagnosed with dementia, stroke or in coma, the Will will not take into effect. For these, you will need Lasting Power of Attorney (LPA) or Advanced Medical Directive (AMD) so that the decision can be assigned to someone when you are in no condition to make.

Can I make my own will?

Yes, you can. But it's not recommend. It's best left to the professional.

E.g. if you owned a Lexus and would like to pass it to your son when you passes on. In your Will, you indicated "to give Lexus car to my son". If you have changed your car to BMW, upon your demise, your executor will need to sell your BMW and purchase a Lexus for your son.

Being smart alec, you rephrase it to "to give a car to my son". But then if you have sold your car and/or bought a yacht, then the executor will need to find monies or sell your yacht to buy a car for your son.

What can I put into the Will?

Basically you can put all your estate in your Will except those governed by the law. Refer to the Cheat Sheet here for quick reference on what can and cannot be distributed by law.

How about estate that is overseas?

Estate is divided into 2 types: Movable and Immovable Estate.

For movable estate such as overseas bank accounts, investment, etc. it can be distributed via your Will locally here.

For immovable estate such as overseas properties, land title, etc. it's best to do up a will at the respective country. Immovable estate are usually governed by the respective country's laws.

Is it possible that my Will be revoked?

Yes, when you marry or re-marry unless it's mentioned in the Will.

How about if I'm divorced?

No, divorce does not revoke your Will. So do update your Will promptly after change in marital status.

To add-on, without a Will, even after you file for divorce, the Intestate Succession Act (where you spouse is entitled to HALF of ALL your properties) continues to apply until the date of Final Judgment.

And your spouse also have the FIRST RIGHT to apply for the letter of the administration from the court to deal with all your estate!

Is the Will best kept in a safe place e.g. Bank Safe?

Yes, it should be kept in a safe place but it's a no no to keep in the Bank Safe. Because no one other than yourself has the access to the Bank Safe. However you can consider keeping it in a "fire proof" safe deposit box at home.

Since the Executor needs it to carry out your Will, it would make sense that the Will should be made known where it is especially for the Executor and/or Beneficiaries. If not, you can consider registering your Will location at the "Will Registry" maintained by the Public Trustee of Singapore.

If the Will cannot be found, then the estate will be distributed based on the The Intestate Succession Act.

Other than Will, anything else I need to consider?

Will is effective only upon death. If one is diagnosed with dementia, stroke or in coma, the Will will not take into effect. For these, you will need Lasting Power of Attorney (LPA) or Advanced Medical Directive (AMD) so that the decision can be assigned to someone when you are in no condition to make.

16 October 2017

[Case Studies] No Will can cost you stamp fees and legal fees on the house

A family consists of a husband, wife and 2 young children. They live in the same HDB house with husband paying and owning the house. The wife and children are just occupier of the house.

When the husband passes on, with no Will, based on The Intestate Succession Act, the wife is entitled to 50% of the house and the 2 children, 25% each. This is entitlement and is not automatically transfer/given. The wife will need to apply to the court for letter of administration to transfer half of the flat to herself and most probably she will also wants to buy over the other half share from their young children.

This will cost the wife tens of thousands of dollars in stamp fees and legal fees for the transfer.

With a Will, the transfer costs only few hundred dollars. And more importantly the process is much faster especially during this devastating period for the family where the wife will not need go through the tedious process of applying for the letter of administration and carry out the paper works.

Note: If the HDB house is owned under "Joint Tenancy" with the wife, then the husband portion will be automatically transferred to the wife. In this case, the Will will not supersede the transfer/allocation.

Recommended Reading on Will:

When the husband passes on, with no Will, based on The Intestate Succession Act, the wife is entitled to 50% of the house and the 2 children, 25% each. This is entitlement and is not automatically transfer/given. The wife will need to apply to the court for letter of administration to transfer half of the flat to herself and most probably she will also wants to buy over the other half share from their young children.

This will cost the wife tens of thousands of dollars in stamp fees and legal fees for the transfer.

With a Will, the transfer costs only few hundred dollars. And more importantly the process is much faster especially during this devastating period for the family where the wife will not need go through the tedious process of applying for the letter of administration and carry out the paper works.

Note: If the HDB house is owned under "Joint Tenancy" with the wife, then the husband portion will be automatically transferred to the wife. In this case, the Will will not supersede the transfer/allocation.

Recommended Reading on Will:

12 September 2017

[Case Study]Pay $60k and receive $550 for life - A Good Deal?

Recently we received this case study using premium financing to pay for a retirement plan.

At age 40, with an initial outlay of $60,000, is able to receive a projected monthly income of $550 (for life). How this works:

Can this really works? We are a bit skeptical as it heavily depends on these 2 main conditions and variables:

1) Non-Guaranteed portion

Guaranteed amount is $275 and the loan amount is $311. So the non-guaranteed portion needs to generate minimally $36 to offset the loan totally.

Only if the insurer able to generate 4.75% return on their participating funds, then one can get the $239 extra.

2) Interest Rate

RHB interest is based on 1.8%. Currently we are at all time low interest rate environment. When interest rates go up, the loan amount will go up as well.

To us, though the retirement plan is good but the premium financing part is risky.

At age 40, with an initial outlay of $60,000, is able to receive a projected monthly income of $550 (for life). How this works:

Can this really works? We are a bit skeptical as it heavily depends on these 2 main conditions and variables:

1) Non-Guaranteed portion

Guaranteed amount is $275 and the loan amount is $311. So the non-guaranteed portion needs to generate minimally $36 to offset the loan totally.

Only if the insurer able to generate 4.75% return on their participating funds, then one can get the $239 extra.

2) Interest Rate

RHB interest is based on 1.8%. Currently we are at all time low interest rate environment. When interest rates go up, the loan amount will go up as well.

To us, though the retirement plan is good but the premium financing part is risky.

31 July 2017

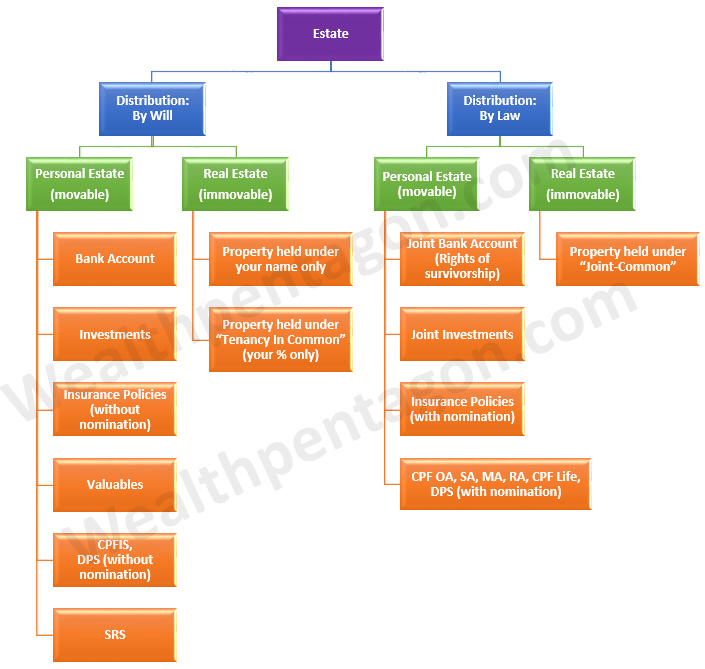

CheatSheet : Estate Distribution

You can easily refer to the cheat sheet below on what can be Will'ed and what can't:

Basically your estate is divided into 2 categories: Those can be distributed by Will and those by Law. Within the categories, each of them is further divided into estate that is movable (like your cash & investment) and those that is immovable (like your properties). All the different estates are listed clearly in their respective categories for your easy reference.

E.g. If you indicate your CPF monies in your Will to be given to so & so, the monies CANNOT be distributed accordingly. Because, by law, CPF monies can only be distributed using the CPF Nomination form.

So have you make your nomination yet? It's free.

30 June 2017

Does everybody have a Will?

As a matter of fact, yes we do. Even we have not visited any lawyer nor wrote anything before. The Will is actually a default Will decided by the government.

Let's talk about what happen the morning "After" death. If there's a Will in place, the person will die testate. If there's no will then the person dies intestate.

If the person dies testate (with a Will), the "appointed" representative (executor) will go to the court and go through the Probate Process and distribute the estate according to the Will.

If the person dies intestate (without a Will), the "agreed" representative will have to go to the court and go through the Administration Process and the distribution will based on the Intestate Succession Act.

Look and sounds the same? Well, not quite. In fact, there's a big difference. Let's see what's the inconvenience if the person dies intestate (without a Will):

1) "Agreed" Representative

Family members will need to agree on who will be the representative which can cause inconvenience and delays. Upon agreement the representative will be need to apply in the court to be the Administrator.

2) Bond & Sureties

Depending on the court, the Administrator might need to provide a bond and sureties (which each sureties asset worth's is same or more than the deceased) especially when there's minor involves.

3) Intestate Succession Act

The distribution can be found here at point no. 6:

https://www.mlaw.gov.sg/content/pto/en/deceased-cpf-estate-monies/information-for-next-of-kin-estate-monies.html

Generally, if the deceased dies leaving Spouse:

- with no children & parents : 100% Spouse

- with children & no parents : 50% Spouse; 50% Children

- with children & parents : 50% Spouse; 50% Children

It's correct. Parents will not get anything, if the deceased dies leaving spouse with children.

Example, husband and child met with an accident and passed away. The husband estate will go to the child and wife; with no estate for the husband's parents. And when the wife passed away, her estate (including her husband's $2 million) will go to her parents.

Without a Will, you cannot determine how your estate is distributed when you passed on and it can end up with the person you dislike.

So will you make a Will?

Let's talk about what happen the morning "After" death. If there's a Will in place, the person will die testate. If there's no will then the person dies intestate.

If the person dies testate (with a Will), the "appointed" representative (executor) will go to the court and go through the Probate Process and distribute the estate according to the Will.

If the person dies intestate (without a Will), the "agreed" representative will have to go to the court and go through the Administration Process and the distribution will based on the Intestate Succession Act.

Look and sounds the same? Well, not quite. In fact, there's a big difference. Let's see what's the inconvenience if the person dies intestate (without a Will):

1) "Agreed" Representative

Family members will need to agree on who will be the representative which can cause inconvenience and delays. Upon agreement the representative will be need to apply in the court to be the Administrator.

2) Bond & Sureties

Depending on the court, the Administrator might need to provide a bond and sureties (which each sureties asset worth's is same or more than the deceased) especially when there's minor involves.

3) Intestate Succession Act

The distribution can be found here at point no. 6:

https://www.mlaw.gov.sg/content/pto/en/deceased-cpf-estate-monies/information-for-next-of-kin-estate-monies.html

Generally, if the deceased dies leaving Spouse:

- with no children & parents : 100% Spouse

- with children & no parents : 50% Spouse; 50% Children

- with children & parents : 50% Spouse; 50% Children

It's correct. Parents will not get anything, if the deceased dies leaving spouse with children.

Example, husband and child met with an accident and passed away. The husband estate will go to the child and wife; with no estate for the husband's parents. And when the wife passed away, her estate (including her husband's $2 million) will go to her parents.

Without a Will, you cannot determine how your estate is distributed when you passed on and it can end up with the person you dislike.

So will you make a Will?

[Newsletter]Which estate cannot be distributed by Will?

Which estate cannot be distributed by Will?

The answer is CPF-OA (Ordinary Account)

The answer is CPF-OA (Ordinary Account)

31 May 2017

[Newsletter]Which estate cannot be distributed by Will?

Which estate cannot be distributed by Will?

o Bank Account

o CPF-OA (Ordinary Account)

o CPF-IS (Investment Scheme)

o Insurance Policies (without nomination)

o Property held under "Tenancy In Common"

Click here to answer this question and the first 10 correct answers will win a USB Mobile fan (for Android)

30 April 2017

[Newsletter]Can your brother/niece claims your Insurance policy(ies)?

The answer is Yes!

This is because if there's no nomination or Will is made, the insurance company may pay up to $150,000 of the policy proceed to any person who is considered as a "proper claimant".

Who is "proper claimant"? They can be any of the deceased's parent, child, brother, sister, nephew, niece, widower or widow.

So, if you have not done your Nomination, please contact your Financial Consultant for it. It's simply filling up of forms and it's FREE.

You might also be interested to check with your Financial Consultant about "Will" & "LPA" where one takes care of your welfare when you are no longer around and the other when should you loose your mental capacity one day.

You can download the latest "Your Guide to the Nomination of Insurance Nominees" from the LIA website here:

http://www.lia.org.sg/node/93

While you are at it, you can also check the unclaimed insurance proceeds here:

http://www.lia.org.sg/consumers/unclaimed-proceeds/list

31 March 2017

[Newsletter]Can your brother/niece claims your Insurance policy(ies)?

Click here to answer this question and the first 10 correct answers will win a USB Mobile fan (for Android)

The answer will be disclosed in our Newsletter next month & more details on such framework will be shared. So, do stay tuned!

7 January 2017

Wealth Distribution

This Wealth Distribution looks at preserving and distributing your estate. The only certainty in life is that it will not last forever. We will help you develop an effective and efficient estate plan so that your legacy will be well preserved and distributed according to your wishes.

Key considerations:

- Will

- CPF Nomination

- Life insurance beneficiaries

- Advance Medical Directive

- Lasting Power of Attorney

2 January 2017

Five Steps of Financial Planning

Basically there are only five steps to a financial planning process:

- Gather & Establish Objective

- Analyse & Evaluate Information

- Develop Plans and Recommendations

- Implement Plans & Recommendations

- Review Periodically

Five Pillars of Wealth

The Five Pillars of Wealth are the essential elements in a comprehensive framework that covers the wealth management needs of an individual from a complete perspective. Every individual who cares about his/her financial life will benefit from this framework whether he/she is just getting by, rich, poor or broke. Later we shall see that dire consequences await those who do not adequately address any of the crucial pillars of wealth management.

- Wealth Maintenance

- Wealth Accumulation

- Wealth Protection & Preservation

- Wealth Enhancement

- Wealth Distribution

Or Wealth M.A.P.P.E.D in short.

Subscribe to:

Posts (Atom)